What is GST input credit?

A key idea in the GST system is the Goods and Services Tax (GST) input credit, or Input Tax Credit (ITC). It enables companies to get a credit for the taxes they have paid on the goods and services they have purchased. By enabling companies to deduct the tax paid on their purchases from the tax received on their sales, it essentially avoids the cascading effect of taxes, in which taxes are imposed on top of taxes.

Table of Contents

The following are the main features of GST input credit:

- Claiming Credit:

- Registered businesses that are liable to pay GST on their sales can claim a credit for the GST paid on their purchases. This credit can be used to offset their tax liability.

- Eligibility:

- To claim GST input credit, the following conditions must be met:

- The business must be registered under GST.

- The business must have a valid tax invoice or document that evidences the GST paid on purchases.

- The supplier of the goods or services must have deposited the GST with the government.

- To claim GST input credit, the following conditions must be met:

- Type of Purchases:

- GST input credit can be claimed on purchases related to business activities. This includes both goods and services. However, there are restrictions on certain categories of goods and services, such as those used for personal consumption or for making exempt supplies.

- Matching and Reconciliation:

- The GST input credit claimed by a business must match the details as reported by its suppliers. This process of matching and reconciliation helps ensure the accuracy of credit claims.

- Utilization of Credit:

- Once a business claims GST input credit, it can use this credit to pay its output tax liability (the tax collected on sales). If there is excess input credit after offsetting the output tax liability, the business can carry it forward to subsequent tax periods or claim a refund.

- Cross-Utilization:

- GST input credit can be cross-utilized for CGST (Central Goods and Services Tax), SGST (State Goods and Services Tax), IGST (Integrated Goods and Services Tax), and cess, depending on the nature of the tax liability.

- Time Limit for Claiming Credit:

- The time limit for claiming GST input credit is typically up to the due date for filing the September return of the following financial year or the filing of the annual return, whichever is earlier.

- Blocked Credits:

- Some categories of GST input credit are blocked or restricted. For example, credit on certain luxury items or services like food and beverages, health and fitness services, and more may be blocked.

- Compliance and Documentation:

- Accurate record-keeping and compliance are essential for claiming GST input credit. Businesses must maintain proper documentation, including invoices and supporting documents, to substantiate their claims.

GST input credit plays a crucial role in simplifying the tax structure and promoting compliance within the GST system. It is designed to ensure that businesses are not burdened with double taxation and can recover the tax they have paid on their purchases, ultimately reducing the overall tax burden on goods and services throughout the supply chain.

What are the rules for GST input credit?

The GST legislation and regulations explain the procedures for claiming input credit for Goods and Services Tax (GST) in India. Businesses must comprehend and abide by these regulations in order to properly claim credit for the GST they have paid on their purchases.

- Valid GST Registration:

- To claim GST input credit, a business must be registered under GST. So file your GST Registation Now.

- Eligible Supplies:

- Input credit can be claimed only on eligible supplies, which include taxable supplies, zero-rated supplies, and exempt supplies where the business is opting for the composition scheme.

- Possession of Tax Invoice:

- The business must have a valid tax invoice or other prescribed documents to support the GST input credit claim. The invoice should include specific details, such as the supplier’s GSTIN, the recipient’s GSTIN, a description of the goods or services, and the amount of GST paid.

- Matching and Reconciliation:

- Input credit claims must match the details provided by the suppliers. The government has implemented a matching mechanism to ensure the accuracy of credit claims.

- Timely Filing of Returns:

- The business should have filed all its GST returns, including GSTR-1 (for outward supplies) and GSTR-3B (for summary returns). Timely filing of returns is crucial to claim input credit.

- Utilization of Credit:

- GST input credit can be utilized to offset the tax liability on output supplies (i.e., tax collected on sales). If there is an excess credit, it can be carried forward or claimed as a refund, subject to certain conditions.

- Blocked Credits:

- Some categories of input credits are blocked or restricted. For example, credit on goods or services used for personal consumption or for making exempt supplies may be blocked.

- Reverse Charge Mechanism:

- If GST is payable under the reverse charge mechanism, the recipient of the goods or services is eligible to claim input credit on the GST paid.

- Apportionment of Credit:

- Businesses that engage in both taxable and non-taxable supplies or supplies to different states must apportion the input credit accordingly.

- ITC on Capital Goods:

- Input credit on capital goods can be claimed, but the credit is typically spread over several tax periods based on prescribed formulas.

- Prescribed Documentation:

- Maintain proper records and documentation to substantiate input credit claims. This includes invoices, receipts, and other relevant documents.

- Time Limit for Claiming Credit:

- The time limit for claiming GST input credit is typically up to the due date for filing the September return of the following financial year or the filing of the annual return, whichever is earlier.

- Matching Offline Tool (MOT):

- In some cases, businesses may be required to use the Matching Offline Tool (MOT) for reconciliation and matching of credit.

- Corrective Measures:

- If discrepancies or errors are identified in previous returns, corrective measures can be taken in subsequent returns.

How to claim GST input credit?

To claim Goods and Services Tax (GST) input credit in India, businesses need to follow specific procedures and meet certain criteria. Here is a step-by-step guide on how to claim GST input credit:

- Eligibility and Registration:

- Ensure that your business is registered under the GST regime, as only registered businesses are eligible to claim input credit.

- Purchase of Eligible Goods and Services:

- Purchase goods or services for your business operations from registered suppliers who charge GST.

- Check the Validity of Tax Invoices:

- Verify that the invoices or other prescribed documents you receive from your suppliers are valid and contain the necessary details. A valid tax invoice should include the supplier’s GSTIN, the recipient’s GSTIN, a description of the goods or services, and the amount of GST paid.

- Ensure Proper Matching:

- Ensure that the details of the invoices you receive match the details as reported by your suppliers. The government has implemented a matching mechanism to verify the accuracy of credit claims.

- File GST Returns:

- Regularly file your GST returns, including GSTR-1 (for outward supplies) and GSTR-3B (for summary returns). Timely filing of returns is essential to claim input credit.

- Complete the Form GSTR-2A:

- Refer to the auto-populated GSTR-2A form, which contains details of your eligible input credit as per the information provided by your suppliers. Review and verify this form.

- Claim the Input Credit:

- Based on the information in GSTR-2A and your own records, claim the eligible input credit in your GSTR-3B return. You can claim the credit for Central Goods and Services Tax (CGST), State Goods and Services Tax (SGST), and Integrated Goods and Services Tax (IGST) based on the nature of the supply.

- Adjustment of Input Credit:

- You can adjust the input credit against the tax liability on your output supplies (i.e., tax collected on sales). For example, you can use CGST input credit to pay CGST liability, SGST input credit to pay SGST liability, and IGST input credit to pay IGST liability.

- Carry Forward or Refund:

- If there is excess input credit after offsetting your tax liability, you can carry it forward and use it in subsequent tax periods. Alternatively, you can apply for a refund of the excess credit, subject to certain conditions and procedures.

- Maintain Proper Records:

- Keep thorough records of all invoices, receipts, and supporting documentation related to your purchases and input credit claims. Proper record-keeping is crucial for compliance and audit purposes.

- Regularly Review and Reconcile:

- Periodically review and reconcile your input credit claims with your supplier’s declarations, as discrepancies may arise. Use the Matching Offline Tool (MOT) if required.

- Comply with Notification Updates:

- Stay updated with the latest notifications and amendments to GST laws and regulations, as rules and procedures may change.

It’s important to note that GST rules and regulations are subject to change, and the process for claiming input credit may have been updated since my last knowledge update in January 2022. Therefore, it’s advisable to consult with a qualified chartered accountant or GST consultant for the most current information and guidance on claiming GST input credit in India.

how to check GST input credit?

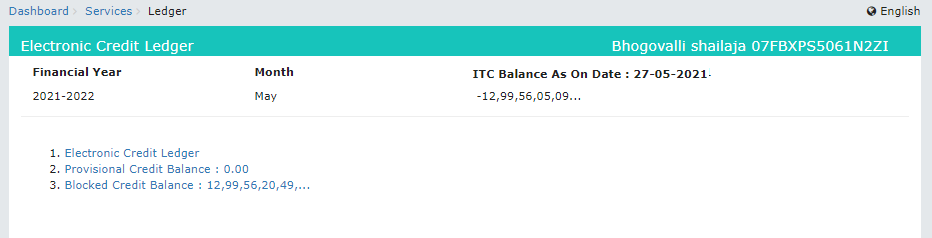

The Electronic Credit Ledger allows taxpayers to view the credit balance as on date as well as Blocked Credit Balance details and Provisional Credit Balance. Follow these steps if you want to know how to check input tax credit in GST portal:

step-1: Access the URL. The GST Home page is displayed. Login to the GST Portal with valid credentials. Click the Services > Ledgers > Electronic Credit Ledger option.

Step-2: The Electronic Credit Ledger page is displayed. The credit balance as on today’s date, Provisional Credit Balance and Blocked Credit Balance is displayed.

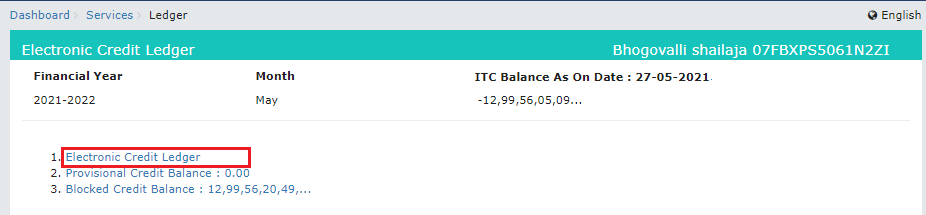

Step-3: Click the Electronic Credit Ledger link. This enables the taxpayer to view various credit ledger related details further.

Note: Negative amounts in Electronic Credit Ledger cannot be utilized for payment of liabilities.

Step-4: Select the From and To date using the calendar to select the period for which you want to view the transactions of Electronic Credit Ledger. Click the GO button.

Step-5: The Electronic Credit Ledger details are displayed.

Items on which Input Tax Credit is not allowed

The input tax credit is not available for claims in the following cases-

- Motor vehicles, with a seating capacity of less than or equal to 13 persons (including the driver), goods transport agencies, vessels and aircraft, except for a few cases. So as an exception, ITC is allowed in the below cases:

- Such motor vehicles and conveyances are further supplied i.e. sold.

- Transport of passengers and goods.

- Conveyance is used for imparting training on driving, flying, and navigating such vehicles or conveyances.

- Services of general insurance, servicing, repair and maintenance relating to motor vehicles, vessels or aircraft in Sl. no.1.

- Food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery.

But if the goods and/or services are taken to deliver the same category of services or as a part of a composite supply, the input tax credit will be available

Example: Mr Dev purchases cosmetic creams to supply it to a customer, then ITC on purchases will be allowed. - Membership in a club, health, and fitness centre.

- Rent-a-cab, health insurance and life insurance except in the following cases where it is allowed:

- Government makes it obligatory for employers to provide it to their employees by law. For example, the mandatory cab services for female staff in night shifts.

- Goods and/or services are taken to deliver the same category of services or as a part of a composite supply, input tax credit will be available.

For example, if Mr Dev takes the service of rent-a-cab to supply to Mr Manoj, a customer, then the ITC on purchases will be allowed. - Leasing, renting or hiring motor vehicles, vessels or aircraft, except cases in Sl.no. 1.

- Travel benefits are extended to employees on vacation such as leave or home travel concessions.

- Works contract service for construction of an immovable property (except plant & machinery or for providing a further supply of works contract service).

- Goods and/or services for the construction of an immovable property whether to be used for personal or business use.

- Goods and/or services where tax has been paid under the composition scheme.

- Goods and/or services used for personal use.

- Goods or services or both are received by a non-resident taxable person except for any of the goods imported by him.

- Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples.

- ITC will not be available in the case of any tax paid due to non-payment or short tax payment, excessive refund or ITC utilised or availed by the reason of fraud or willful misstatements or suppression of facts or confiscation and seizure of goods.

- Special cases: Standalone restaurants will charge only 5% GST but cannot enjoy any ITC on the inputs.

- The expenditure spent on Corporate Social Responsibility (CSR) initiatives by corporates.